Kiva Project

Contents

Kiva Project#

(adapted from https://bit.ly/2J7G9f8)

PROBLEM:#

Context#

Kiva.org is an online crowdfunding platform to extend financial services to poor and financially excluded people around the world. Kiva lenders have provided over $1 billion dollars in loans to over 2 million people.

In order to set investment priorities, help inform lenders, and understand their target communities, knowing the level of poverty of each borrower is critical. However, this requires inference based on a limited set of information for each borrower.

Submissions in this challenge will take the form of Python data analysis.

Kiva has provided a dataset of loans issued over the 2014-2018 time period, and participants are invited to use this data as well as source external public datasets to help Kiva build models for assessing borrower welfare levels. With a stronger understanding of their borrowers and their poverty levels, Kiva will be able to better assess and maximize the impact of their work.

Problem statement#

For the locations in which Kiva has active loans, the objective is to pair Kiva’s data with additional data sources to estimate the welfare level of borrowers in specific regions, based on shared economic and demographic characteristics.

A good solution would connect the features of each loan or product to one of several poverty mapping datasets, which indicate the average level of welfare in a region on as granular a level as possible. Many datasets indicate the poverty rate in a given area, with varying levels of granularity. Kiva would like to be able to disaggregate these regional averages by gender, sector, or borrowing behavior in order to estimate a Kiva borrower’s level of welfare using all of the relevant information about them. Strong submissions will attempt to map vaguely described locations to more accurate geocodes.

Personal disclaimer#

From a research perspective, the results obtained are never going to be a full representation of the realities that borrowers experience. It is meant to spark a discussion around how we can identify the welfare level of borrowers and improve them where we can.

SOLUTION:#

Python Packages & Functions#

Here we upload all the Python packages and datasets required for analysis.

# Packages

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

Data#

1. Original Data#

loan_data = pd.read_csv('C://Users//CT//Documents//GitHub//knowledge-hub//book//data//kiva-project//kiva_loans.csv')

location_data = pd.read_csv('C://Users//CT//Documents//GitHub//knowledge-hub//book//data//kiva-project//kiva_mpi_region_locations.csv')

loan_themes = pd.read_csv('C://Users//CT//Documents//GitHub//knowledge-hub//book//data//kiva-project//loan_theme_ids.csv')

regional_lts = pd.read_csv('C://Users//CT//Documents//GitHub//knowledge-hub//book//data//kiva-project//loan_themes_by_region.csv')

dfs = {'loan_data':loan_data, 'location_data':location_data,

'loan_themes':loan_themes, 'regional_lts':regional_lts}

for key, val in dfs.items():

print(str(key+' shape:'), val.shape)

loan_data shape: (671205, 20)

location_data shape: (2772, 9)

loan_themes shape: (779092, 4)

regional_lts shape: (15736, 21)

Descriptions of the original datasets

There are four data sources provided by Kiva:

loan_data

id - Unique ID for loan

funded_amount - The amount disbursed by Kiva to the field agent (USD)

loan_amount - The amount disbursed by the field agent to the borrower (USD)

activity - More granular category

sector - High level category

use - Exact usage of loan amount

country_code - ISO country code of country in which loan was disbursed

country - Full country name of country in which loan was disbursed

region - Full region name within the country

currency - The currency in which the loan was disbursed

partner_id - ID of partner organization

posted_time - The time at which the loan is posted on Kiva by the field agent

disbursed_time - The time at which the loan is disbursed by the field agent to the borrower

funded_time - The time at which the loan posted to Kiva gets funded by lenders completely

term_in_months - The duration for which the loan was disbursed in months

lender_count - The total number of lenders that contributed to this loan

tags

borrower_genders - Comma separated M,F letters, where each instance represents a single male/female in the group

repayment_interval

date

location_data

LocationName - region, country

ISO - some sort of unique abbreviation for country

country - country

region - region within country

world_region - parts of the world

MPI - multidimensional poverty index

geo - (latitude, longitude)

lat - latitude

lon - longitude

loan_themes

id - Unique ID for loan (Loan ID)

Loan Theme ID - ID for Loan Theme

Loan Theme Type - Category name of type of loan

Partner ID

regional_lts

Partner ID

Field Partner Name

sector

Loan Theme ID

Loan Theme Type

country

forkiva

region

geocode_old

ISO

number

amount

LocationName

geocode

names

geo

lat

lon

mpi_region

mpi_geo

rural_pct

2. Supplementary Data#

In this section, we aim to gather the following data from the World Bank:

Per Capita Expenditure (PCE) for each country - this is the total market value of all purchases in a country divided by that country’s total population (data: https://bit.ly/3blw0be)

# Per Capita Expenditure

PCE_data = pd.read_csv('C://Users//CT//Documents//GitHub//knowledge-hub//book//data//kiva-project//PCE data.tsv', sep='\t')

print('PCE data shape:',PCE_data.shape)

PCE_data = PCE_data.drop(['Unnamed: 61'],axis=1) # dropping the column containing only NaN values

PCE data shape: (185, 62)

# add this dataset to the dictionary

dfs['PCE_data'] = PCE_data

dfs.keys()

dict_keys(['loan_data', 'location_data', 'loan_themes', 'regional_lts', 'PCE_data'])

Data Summary#

for key, val in dfs.items():

# 1. Get the summary table

num_summary = val.describe()

cat_summary = val.loc[:,val.dtypes==np.object].describe(include=['O'])

# 2. Display it

print('\nSUMMARY STATISTICS WITHOUT AGGREGATION: {}'.format(key),'\n')

display(num_summary)

print('\n')

display(cat_summary)

print('\n')

SUMMARY STATISTICS WITHOUT AGGREGATION: loan_data

| id | funded_amount | loan_amount | partner_id | term_in_months | lender_count | |

|---|---|---|---|---|---|---|

| count | 6.712050e+05 | 671205.000000 | 671205.000000 | 657698.000000 | 671205.000000 | 671205.000000 |

| mean | 9.932486e+05 | 785.995061 | 842.397107 | 178.199616 | 13.739022 | 20.590922 |

| std | 1.966113e+05 | 1130.398941 | 1198.660073 | 94.247581 | 8.598919 | 28.459551 |

| min | 6.530470e+05 | 0.000000 | 25.000000 | 9.000000 | 1.000000 | 0.000000 |

| 25% | 8.230720e+05 | 250.000000 | 275.000000 | 126.000000 | 8.000000 | 7.000000 |

| 50% | 9.927800e+05 | 450.000000 | 500.000000 | 145.000000 | 13.000000 | 13.000000 |

| 75% | 1.163653e+06 | 900.000000 | 1000.000000 | 204.000000 | 14.000000 | 24.000000 |

| max | 1.340339e+06 | 100000.000000 | 100000.000000 | 536.000000 | 158.000000 | 2986.000000 |

| activity | sector | use | country_code | country | region | currency | posted_time | disbursed_time | funded_time | tags | borrower_genders | repayment_interval | date | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 671205 | 671205 | 666973 | 671197 | 671205 | 614405 | 671205 | 671205 | 668809 | 622874 | 499789 | 666984 | 671205 | 671205 |

| unique | 163 | 15 | 424912 | 86 | 87 | 12695 | 67 | 667399 | 5719 | 498007 | 86719 | 11298 | 4 | 1298 |

| top | Farming | Agriculture | to buy a water filter to provide safe drinking... | PH | Philippines | Kaduna | PHP | 2017-05-15 00:00:00+00:00 | 2017-02-01 08:00:00+00:00 | 2016-09-21 13:03:24+00:00 | user_favorite | female | monthly | 2017-03-20 |

| freq | 72955 | 180302 | 5217 | 160441 | 160441 | 10000 | 160440 | 25 | 2800 | 33 | 27088 | 426502 | 342717 | 1308 |

SUMMARY STATISTICS WITHOUT AGGREGATION: location_data

| MPI | lat | lon | |

|---|---|---|---|

| count | 984.000000 | 892.000000 | 892.000000 |

| mean | 0.211330 | 9.169710 | 16.635888 |

| std | 0.183621 | 16.484531 | 61.234566 |

| min | 0.000000 | -34.947896 | -122.747131 |

| 25% | 0.053000 | -1.027901 | -12.819854 |

| 50% | 0.155000 | 11.211379 | 26.419389 |

| 75% | 0.341500 | 18.084292 | 47.019436 |

| max | 0.744000 | 49.264748 | 138.581284 |

| LocationName | ISO | country | region | world_region | geo | |

|---|---|---|---|---|---|---|

| count | 984 | 1008 | 1008 | 984 | 1008 | 2772 |

| unique | 984 | 102 | 102 | 928 | 6 | 881 |

| top | Badakhshan, Afghanistan | NGA | Nigeria | Central | Sub-Saharan Africa | (1000.0, 1000.0) |

| freq | 1 | 37 | 37 | 8 | 432 | 1880 |

SUMMARY STATISTICS WITHOUT AGGREGATION: loan_themes

| id | Partner ID | |

|---|---|---|

| count | 7.790920e+05 | 764279.000000 |

| mean | 1.047475e+06 | 180.825840 |

| std | 2.282538e+05 | 97.914029 |

| min | 6.386310e+05 | 9.000000 |

| 25% | 8.499768e+05 | 126.000000 |

| 50% | 1.046528e+06 | 145.000000 |

| 75% | 1.244768e+06 | 204.000000 |

| max | 1.444243e+06 | 557.000000 |

| Loan Theme ID | Loan Theme Type | |

|---|---|---|

| count | 764279 | 764279 |

| unique | 956 | 203 |

| top | a1050000000wf0q | General |

| freq | 110264 | 380693 |

SUMMARY STATISTICS WITHOUT AGGREGATION: regional_lts

| Partner ID | number | amount | lat | lon | rural_pct | |

|---|---|---|---|---|---|---|

| count | 15736.000000 | 15736.000000 | 1.573600e+04 | 13662.000000 | 13662.000000 | 14344.000000 |

| mean | 191.376144 | 53.628432 | 2.003991e+04 | 14.328878 | 29.433569 | 68.084635 |

| std | 118.705003 | 403.079799 | 9.636941e+04 | 16.757689 | 83.255739 | 26.550064 |

| min | 9.000000 | 1.000000 | 2.500000e+01 | -34.610548 | -172.790661 | 0.000000 |

| 25% | 123.000000 | 1.000000 | 9.500000e+02 | 6.266728 | -71.967463 | 60.000000 |

| 50% | 154.000000 | 4.000000 | 2.600000e+03 | 13.484101 | 41.899993 | 73.000000 |

| 75% | 217.000000 | 15.000000 | 8.750000e+03 | 22.189940 | 106.677321 | 85.000000 |

| max | 545.000000 | 22538.000000 | 4.929900e+06 | 51.314017 | 159.972900 | 100.000000 |

| Field Partner Name | sector | Loan Theme ID | Loan Theme Type | country | forkiva | region | geocode_old | ISO | LocationName | geocode | names | geo | mpi_region | mpi_geo | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 15736 | 15736 | 15736 | 15736 | 15736 | 15736 | 15736 | 1200 | 15722 | 15736 | 13662 | 13661 | 15736 | 15722 | 9671 |

| unique | 302 | 11 | 718 | 170 | 79 | 2 | 9526 | 340 | 77 | 9561 | 6557 | 6275 | 6558 | 392 | 335 |

| top | Alalay sa Kaunlaran (ASKI) | General Financial Inclusion | a1050000000wf0V | General | Philippines | No | Chouf | (-1.2833333, 36.8166667) | PHL | Chouf, Lebanon | [(19.7126764, 105.8393447)] | Philippines | (1000.0, 1000.0) | Northern Mindanao, Philippines | (8.020163499999999, 124.6856509) |

| freq | 1207 | 13679 | 1152 | 5661 | 3467 | 13211 | 25 | 20 | 3467 | 25 | 43 | 137 | 2074 | 1174 | 1174 |

SUMMARY STATISTICS WITHOUT AGGREGATION: PCE_data

| Country | 1960 | 1961 | 1962 | 1963 | 1964 | 1965 | 1966 | 1967 | 1968 | ... | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 185 | 43 | 44 | 45 | 45 | 47 | 50 | 51 | 52 | 52 | ... | 178 | 164 | 163 | 162 | 160 | 158 | 157 | 156 | 152 | 137 |

| unique | 185 | 43 | 44 | 45 | 45 | 47 | 50 | 51 | 52 | 52 | ... | 178 | 164 | 163 | 162 | 160 | 158 | 157 | 156 | 152 | 137 |

| top | East Asia and Pacific | 358.28 | 376.28 | 391.98 | 366.59 | 359.69 | 358.46 | 343.77 | 364.11 | 386.75 | ... | 7,168.46 | 6,887.91 | 6,766.62 | 6,988.29 | 7,035.26 | 7,013.70 | 7,098.35 | 7,113.80 | 7,152.70 | 923.25 |

| freq | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | ... | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

4 rows × 61 columns

| Country | 1960 | 1961 | 1962 | 1963 | 1964 | 1965 | 1966 | 1967 | 1968 | ... | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 185 | 43 | 44 | 45 | 45 | 47 | 50 | 51 | 52 | 52 | ... | 178 | 164 | 163 | 162 | 160 | 158 | 157 | 156 | 152 | 137 |

| unique | 185 | 43 | 44 | 45 | 45 | 47 | 50 | 51 | 52 | 52 | ... | 178 | 164 | 163 | 162 | 160 | 158 | 157 | 156 | 152 | 137 |

| top | East Asia and Pacific | 358.28 | 376.28 | 391.98 | 366.59 | 359.69 | 358.46 | 343.77 | 364.11 | 386.75 | ... | 7,168.46 | 6,887.91 | 6,766.62 | 6,988.29 | 7,035.26 | 7,013.70 | 7,098.35 | 7,113.80 | 7,152.70 | 923.25 |

| freq | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | ... | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 1 |

4 rows × 61 columns

Exploratory Data Analysis#

The impact of KIVA donors#

In this section, we seek to explore the data to answer certain questions around KIVA donor contributions.

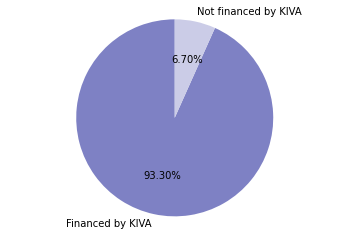

1. How much of the total loan amount has Kiva financed?

# 1. Calculate the percentage of loan requests that have been funded

percentage1 = (loan_data.funded_amount.sum()/loan_data.loan_amount.sum())*100

percentage1 = round(percentage1, 2)

# 2. Display the result

status = ['Financed by KIVA','Not financed by KIVA']

values = [percentage1, (100-percentage1)]

fig1, ax1 = plt.subplots()

ax1.pie(values, labels=status,

autopct='%1.2f%%',

startangle=90,

colors=np.array(['#7e81c4','#cbcce7']))

ax1.axis('equal') # Equal aspect ratio ensures that pie is drawn as a circle.

plt.show()

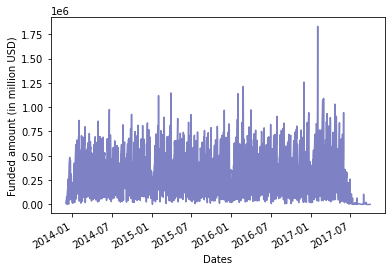

2. How much money have Kiva donors contributed over time?

print('\n', 'DAILY CONTRIBUTIONS OF KIVA DONORS AS A COLLECTIVE')

# convert datetime values to appropriate formats

loan_data['posted_time'] = loan_data['posted_time'].astype('datetime64')

loan_data['disbursed_time'] = loan_data['disbursed_time'].astype('datetime64')

loan_data['funded_time'] = loan_data['funded_time'].astype('datetime64')

# pick out dates

loan_data.loc[:,'disbursement_date'] = loan_data['disbursed_time'].dt.date

# create a pivot-table

tab1 = pd.pivot_table(loan_data, values='funded_amount', index=['disbursement_date'], aggfunc='sum')

# plot this table

from pandas.plotting import register_matplotlib_converters

register_matplotlib_converters()

fig, ax = plt.subplots()

ax.plot(tab1.index, tab1['funded_amount'], color='#7e81c4')

# rotate and align the tick labels so they look better

fig.autofmt_xdate()

# declare the title and show the completed graph

plt.xlabel('Dates')

plt.ylabel('Funded amount (in million USD)')

plt.show()

DAILY CONTRIBUTIONS OF KIVA DONORS AS A COLLECTIVE

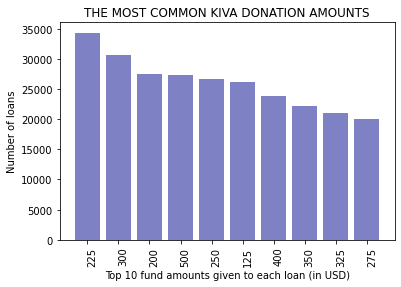

3. How much money have Kiva donors given to individual loans?

# create a pivot-table

loan_count_per_funded_amount = pd.pivot_table(loan_data, values='id', index=['funded_amount'], aggfunc='count')

# rename the column

loan_count_per_funded_amount.columns = ['number_of_loans']

# sort the results in descending order

loan_count_per_funded_amount = loan_count_per_funded_amount.sort_values(by=['number_of_loans'], ascending=False)

# and display top 10 results

amounts = ['225','300','200','500','250','125','400','350','325','275']

fig, ax = plt.subplots()

ax.bar(amounts,loan_count_per_funded_amount.iloc[0:10,0],color='#7e81c4')

plt.ylabel('Number of loans')

ax.set_xticklabels(labels=amounts, rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Top 10 fund amounts given to each loan (in USD)')

plt.title('THE MOST COMMON KIVA DONATION AMOUNTS')

plt.show()

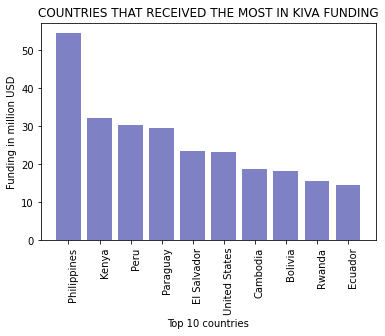

4. How much money have Kiva donors given to individual countries?

# create a pivot-table

tab2 = pd.pivot_table(loan_data, values='funded_amount', index=['country'], aggfunc='sum')

# sort the results in descending order

tab2 = tab2.sort_values(by=['funded_amount'], ascending=False)

# rename the aggregated column to an appropiate label

tab2.columns = ['sum_of_funded_amount']

# make some index entries into columns

tab2 = tab2.reset_index(level=['country'])

# and display top 10 results

fig, ax = plt.subplots()

ax.bar(tab2.iloc[0:10,0],(tab2.iloc[0:10,1]/1000000),color='#7e81c4')

plt.ylabel('Funding in million USD')

ax.set_xticklabels(labels=tab2.iloc[0:10,0], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Top 10 countries')

plt.title('COUNTRIES THAT RECEIVED THE MOST IN KIVA FUNDING')

plt.show()

# create a pivot-table

loans_per_country = pd.pivot_table(loan_data, values='id', index=['country'], aggfunc='count')

# sort the results in descending order

loans_per_country = loans_per_country.sort_values(by=['id'], ascending=False)

# rename the aggregated column to an appropiate label

loans_per_country.columns = ['number_of_loans']

# make some index entries into columns

loans_per_country = loans_per_country.reset_index(level=['country'])

# and display top 10 results

loans_per_country.head(10)

# and display top 10 results

fig, ax = plt.subplots()

ax.bar(loans_per_country.iloc[0:10,0],loans_per_country.iloc[0:10,1],color='#7e81c4')

plt.ylabel('Number of loans')

ax.set_xticklabels(labels=tab2.iloc[0:10,0], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Top 10 countries')

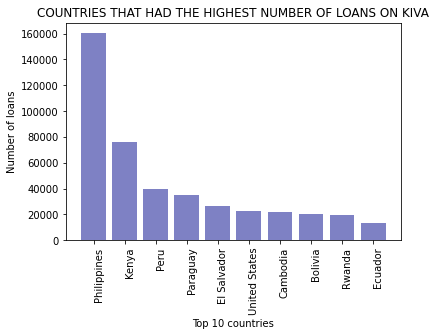

plt.title('COUNTRIES THAT HAD THE HIGHEST NUMBER OF LOANS ON KIVA')

plt.show()

This shows that the top 10 countries in terms of the number of loans and amount of funding from KIVA were the same and each country maintained its position.

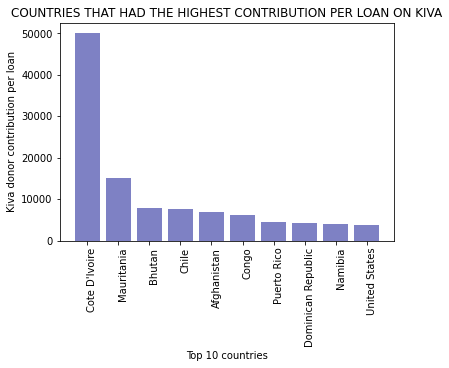

Countries that had the highest contribution per loan were:

# initial status message

print('The shape of tab2 before merge: ', tab2.shape)

# join the data, keeping only relevant entries

tab2 = tab2.merge(loans_per_country, on='country')

# final status message

print('The shape of tab2 after merge: ', tab2.shape)

The shape of tab2 before merge: (87, 2)

The shape of tab2 after merge: (87, 3)

# add a calculated column to the newly merged tab2

tab2.loc[:, 'contribution_per_loan'] = tab2['sum_of_funded_amount']/tab2['number_of_loans']

# sort the results in descending order

tab2 = tab2.sort_values(by=['contribution_per_loan'], ascending=False)

# and display top 10 results

fig, ax = plt.subplots()

ax.bar(tab2.iloc[0:10,0], round(tab2.iloc[0:10,3], 2), color='#7e81c4')

plt.ylabel('Kiva donor contribution per loan')

ax.set_xticklabels(labels=tab2.iloc[0:10,0], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Top 10 countries')

plt.title('COUNTRIES THAT HAD THE HIGHEST CONTRIBUTION PER LOAN ON KIVA')

plt.show()

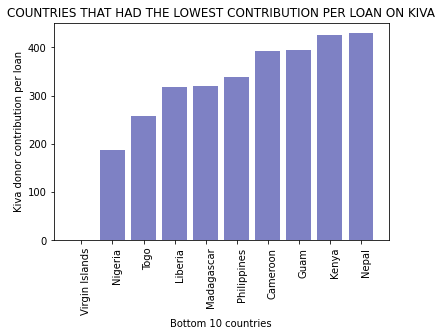

Countries that had the lowest contribution per loan were:

# add a calculated column to the newly merged tab2

tab2.loc[:, 'contribution_per_loan'] = tab2['sum_of_funded_amount']/tab2['number_of_loans']

# sort the results in ascending order

tab2 = tab2.sort_values(by=['contribution_per_loan'], ascending=True)

# and display top 10 results

fig, ax = plt.subplots()

ax.bar(tab2.iloc[0:10,0], round(tab2.iloc[0:10,3], 2), color='#7e81c4')

plt.ylabel('Kiva donor contribution per loan')

ax.set_xticklabels(labels=tab2.iloc[0:10,0], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Bottom 10 countries')

plt.title('COUNTRIES THAT HAD THE LOWEST CONTRIBUTION PER LOAN ON KIVA')

plt.show()

5. What is the geographical footprint of where funds given by KIVA donors end up?

# make a copy of the loan_data dataset and combine it with partner data

loan_data_copy = loan_data.copy()

# ensure that the common column is the same datatype and they share the same name

# the datatype chosen was float64 to preserve any decimal points

print(loan_data_copy.iloc[:,10].name) # original name; stays the same

print('')

print(regional_lts.iloc[:,0].name) #original name - will be changed

#change column name

regional_lts.columns = ['partner_id', 'Field Partner Name', 'sector',

'Loan Theme ID', 'Loan Theme Type', 'country',

'forkiva', 'region', 'geocode_old',

'ISO', 'number', 'amount',

'LocationName', 'geocode', 'names',

'geo', 'lat', 'lon',

'mpi_region', 'mpi_geo', 'rural_pct']

# confirm change

print(regional_lts.iloc[:,0].name)

# change the datatype

regional_lts.iloc[:,0] = regional_lts.iloc[:,0].astype('float64')

partner_id

Partner ID

partner_id

# create a pivot-table

tab3 = pd.pivot_table(loan_data_copy, values='funded_amount', index=['partner_id'], aggfunc='sum')

# sort the results in descending order

tab3 = tab3.sort_values(by=['funded_amount'], ascending=False)

# rename the aggregated column to an appropiate label

tab3.columns = ['sum_of_funded_amount']

# make some index entries into columns

tab3 = tab3.reset_index(level=['partner_id'])

# create another pivot-table

tab4 = pd.pivot_table(regional_lts, values='amount',

index=['partner_id', 'Field Partner Name',

'country'],

aggfunc='count')

# sort the results in descending order

tab4 = tab4.sort_values(by=['amount'], ascending=False)

# rename the aggregated column to an appropiate label

tab4.columns = ['count_of_amount']

# make some index entries into columns

tab4 = tab4.reset_index(level=['partner_id', 'Field Partner Name', 'country'])

# create a third pivot-table

tab5 = pd.pivot_table(loan_data_copy, values='id', index=['partner_id'], aggfunc='count')

# sort the results in descending order

tab5 = tab5.sort_values(by=['id'], ascending=False)

# rename the aggregated column to an appropiate label

tab5.columns = ['number_of_loans']

# make some index entries into columns

tab5 = tab5.reset_index(level=['partner_id'])

# initial status message

print('The shape of tab3 before merge: ', tab3.shape)

# join the data, keeping only relevant entries

tab3 = tab3.merge(tab5, on='partner_id')

# final status message

print('The shape of tab3 after merge: ', tab3.shape)

# initial status message

print('The shape of tab3 before merge: ', tab3.shape)

# join the data, keeping only relevant entries

tab3 = tab3.merge(tab4, on='partner_id')

# final status message

print('The shape of tab3 after merge: ', tab3.shape)

percentage2 = tab3.shape[0]/366 * 100

percentage2 = round(percentage2, 0)

print('Out of the 366 partners that disbursed loans, KIVA had the contact details of '+str(percentage2)+'% of them.')

The shape of tab3 before merge: (366, 2)

The shape of tab3 after merge: (366, 3)

The shape of tab3 before merge: (366, 3)

The shape of tab3 after merge: (331, 6)

Out of the 366 partners that disbursed loans, KIVA had the contact details of 90.0% of them.

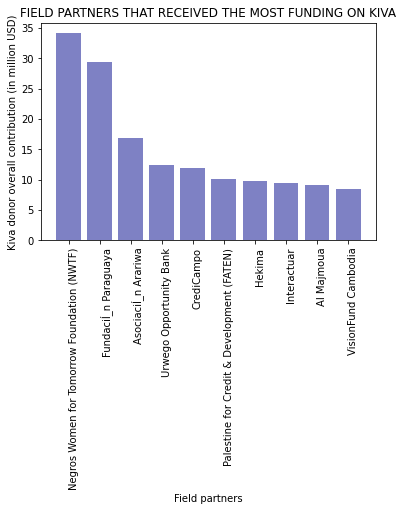

The partners that received the most funding by KIVA were:

# to have more details of the partners that received the most funding by KIVA,

# sort the results in descending order

tab3 = tab3.sort_values(by=['sum_of_funded_amount'], ascending=False)

# drop the unecessary columns

tab3 = tab3.drop('count_of_amount',1)

# display top 10 results; do they match with the original tab3? They match!

fig, ax = plt.subplots()

ax.bar(tab3.iloc[0:10,3], (tab3.iloc[0:10,1]/1000000), color='#7e81c4')

plt.ylabel('Kiva donor overall contribution (in million USD)')

ax.set_xticklabels(labels=tab3.iloc[0:10,3], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Field partners')

plt.title('FIELD PARTNERS THAT RECEIVED THE MOST FUNDING ON KIVA')

plt.show()

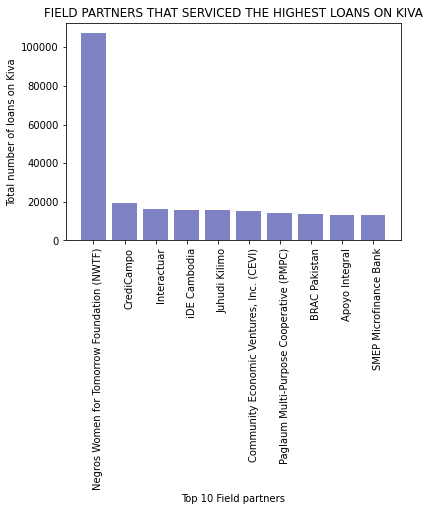

The partners that serviced the highest number of loans on KIVA were:

# sort the results in descending order

tab3 = tab3.sort_values(by=['number_of_loans'], ascending=False)

# display top 10 results in terms of number of loans

fig, ax = plt.subplots()

ax.bar(tab3.iloc[0:10,3], tab3.iloc[0:10,2], color='#7e81c4')

plt.ylabel('Total number of loans on Kiva')

ax.set_xticklabels(labels=tab3.iloc[0:10,3], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Top 10 Field partners')

plt.title('FIELD PARTNERS THAT SERVICED THE HIGHEST LOANS ON KIVA')

plt.show()

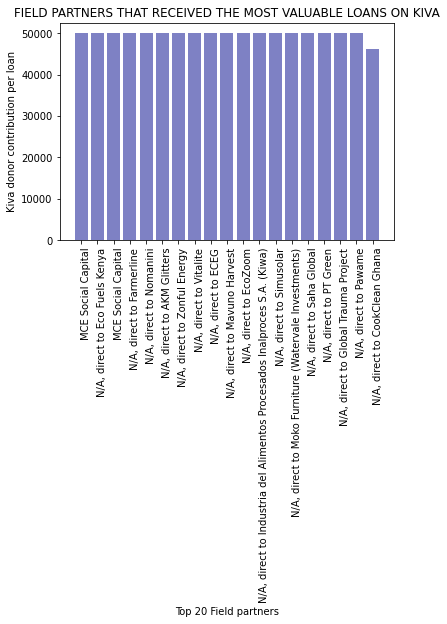

# add a calculated column to the newly merged tab3

tab3.loc[:, 'contribution_per_loan'] = tab3['sum_of_funded_amount']/tab3['number_of_loans']

# sort the results in descending order

tab3 = tab3.sort_values(by=['contribution_per_loan'], ascending=False)

# display top 20 results in terms of donor contribution per loan

fig, ax = plt.subplots()

ax.bar(tab3.iloc[0:20,3], tab3.iloc[0:20,5], color='#7e81c4')

plt.ylabel('Kiva donor contribution per loan')

ax.set_xticklabels(labels=tab3.iloc[0:20,3], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Top 20 Field partners')

plt.title('FIELD PARTNERS THAT RECEIVED THE MOST VALUABLE LOANS ON KIVA')

plt.show()

The per capita contribution shows most of the largest contributions per loan actually went directly to social impact businesses.

The characteristics of KIVA borrowers#

In this section, we seek to understand KIVA borrower characteristics.

1. What is the size of the shortfall for each individual borrower in a given sector?

# create a pivot-table

tab6 = pd.pivot_table(loan_data_copy, values='funded_amount', index=['sector'], aggfunc='sum')

# sort the results in descending order

tab6 = tab6.sort_values(by=['funded_amount'], ascending=False)

# rename the aggregated column to an appropiate label

tab6.columns = ['sum_of_funded_amount']

# make some index entries into columns

tab6 = tab6.reset_index(level=['sector'])

# create another pivot-table

loans_by_sector = pd.pivot_table(loan_data_copy, values='id', index=['sector'], aggfunc='count')

# sort the results in descending order

loans_by_sector = loans_by_sector.sort_values(by=['id'], ascending=False)

# rename the aggregated column to an appropiate label

loans_by_sector.columns = ['number_of_loans']

# make some index entries into columns

loans_by_sector = loans_by_sector.reset_index(level=['sector'])

# create a third pivot-table

loan_amounts_by_sector = pd.pivot_table(loan_data_copy, values='loan_amount', index=['sector'], aggfunc='sum')

# sort the results in descending order

loan_amounts_by_sector = loan_amounts_by_sector.sort_values(by=['loan_amount'], ascending=False)

# rename the aggregated column to an appropiate label

loan_amounts_by_sector.columns = ['sum_of_loan_amount']

# make some index entries into columns

loan_amounts_by_sector = loan_amounts_by_sector.reset_index(level=['sector'])

# initial status message

print('The shape of tab6 before merge: ', tab6.shape)

# join the data, keeping only relevant entries

tab6 = tab6.merge(loans_by_sector, on='sector')

# final status message

print('The shape of tab6 after merge: ', tab6.shape)

# initial status message

print('The shape of tab6 before merge: ', tab6.shape)

# join the data, keeping only relevant entries

tab6 = tab6.merge(loan_amounts_by_sector, on='sector')

# final status message

print('The shape of tab6 after merge: ', tab6.shape)

The shape of tab6 before merge: (15, 2)

The shape of tab6 after merge: (15, 3)

The shape of tab6 before merge: (15, 3)

The shape of tab6 after merge: (15, 4)

# assess additional metrics

tab6.loc[:, 'donor_contribution_per_loan'] = tab6['sum_of_funded_amount']/tab6['number_of_loans']

tab6.loc[:, 'funding_gap_per_loan'] = (-tab6['sum_of_loan_amount']+tab6['sum_of_funded_amount'])/tab6['number_of_loans']

# sort the results in descending order

tab6 = tab6.sort_values(by=['donor_contribution_per_loan'], ascending=False)

# display all results

fig, ax = plt.subplots()

ax.bar(tab6.iloc[:,0], tab6.iloc[:,4], color='#7e81c4')

plt.ylabel('Kiva donor contribution per loan')

ax.set_xticklabels(labels=tab6.iloc[:,0], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Sectors')

plt.title('SECTORS THAT RECEIVED THE MOST VALUABLE LOANS ON KIVA')

plt.show()

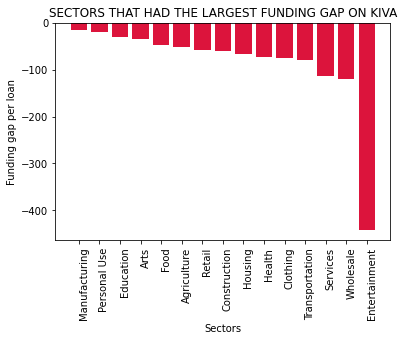

# sort the results in descending order

tab6 = tab6.sort_values(by=['funding_gap_per_loan'], ascending=False)

# display all results

fig, ax = plt.subplots()

ax.bar(tab6.iloc[:,0], tab6.iloc[:,5], color='crimson')

plt.ylabel('Funding gap per loan')

ax.set_xticklabels(labels=tab6.iloc[:,0], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Sectors')

plt.title('SECTORS THAT HAD THE LARGEST FUNDING GAP ON KIVA')

plt.show()

In as much as Entertainment has the second most valuable loans, it appears that this sector had the highest funding gap. Manufacturing had the lowest funding gap.

2. How were loans and funding distributed across the genders?

loan_data_copy.loc[:, 'number_of_all_borrowers'] = loan_data_copy['borrower_genders'].str.count('male') # counts both instances of female and male - they share the 'male' element

loan_data_copy.loc[:, 'number_of_female_borrowers'] = loan_data_copy['borrower_genders'].str.count('female')

loan_data_copy.loc[:, 'number_of_male_borrowers'] = loan_data_copy['number_of_all_borrowers'] - loan_data_copy['number_of_female_borrowers']

print('We had borrower data on',

round(loan_data_copy['number_of_all_borrowers'].count()/loan_data_copy.shape[0]*100, 2),

'% of the loans recorded')

We had borrower data on 99.37 % of the loans recorded

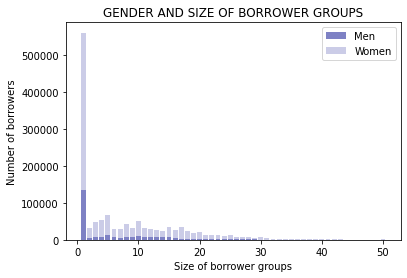

How different genders group together to borrow on Kiva

# create a pivot-table

borrower_group_data = pd.pivot_table(loan_data_copy, values=['number_of_male_borrowers', 'number_of_female_borrowers'],

index=['number_of_all_borrowers'],aggfunc='sum')

#N/B: Using the count gives the total number of loans with borrower data; we need the sum to see the gender distribution across group size

# make some index entries into columns

borrower_group_data = borrower_group_data.reset_index(level=['number_of_all_borrowers'])

# display the results

fig, ax = plt.subplots()

ax.bar(borrower_group_data.iloc[:,0], borrower_group_data.iloc[:,2],

label='Men', color='#7e81c4')

ax.bar(borrower_group_data.iloc[:,0], borrower_group_data.iloc[:,1],

bottom=borrower_group_data.iloc[:,2], label='Women', color='#cbcce7')

ax.set_ylabel('Number of borrowers')

ax.set_xlabel('Size of borrower groups')

ax.set_title('GENDER AND SIZE OF BORROWER GROUPS')

ax.legend()

plt.show()

The graph above shows that most people preferred to borrow as individuals; however, there were substantially larger numbers of women in each group size compared to men.

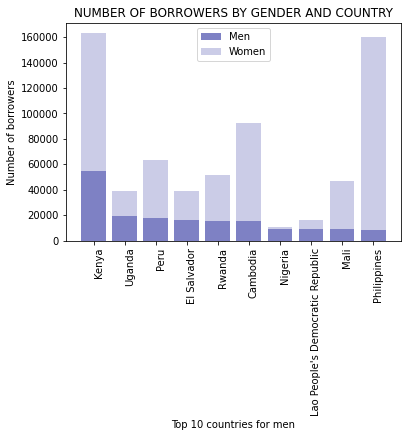

Most common nationalities for the different genders

# create a pivot-table

borrower_country_data = pd.pivot_table(loan_data_copy, values=['number_of_male_borrowers', 'number_of_female_borrowers'],

index=['country'],aggfunc='sum')

# sort the male results in descending order

borrower_country_data = borrower_country_data.sort_values(by=['number_of_male_borrowers'], ascending=False)

# make some index entries into columns

borrower_country_data = borrower_country_data.reset_index(level=['country'])

# display the results

fig, ax = plt.subplots()

ax.bar(borrower_country_data.iloc[0:10,0], borrower_country_data.iloc[0:10,2],

label='Men', color='#7e81c4')

ax.bar(borrower_country_data.iloc[0:10,0], borrower_country_data.iloc[0:10,1],

bottom=borrower_country_data.iloc[0:10,2], label='Women', color='#cbcce7')

ax.set_xticklabels(labels=borrower_country_data.iloc[0:10,0], rotation = (90), fontsize = 10, va='top', ha='left')

ax.set_ylabel('Number of borrowers')

ax.set_xlabel('Top 10 countries for men')

ax.set_title('NUMBER OF BORROWERS BY GENDER AND COUNTRY')

ax.legend()

plt.show()

The country with the highest number of male borrowers was Kenya, while the country where men formed the majority of KIVA borrowers was Nigeria.

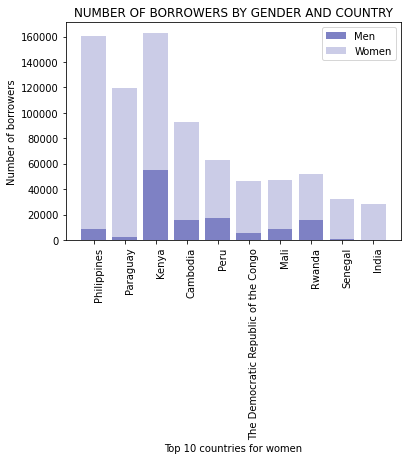

# sort the female results in descending order

borrower_country_data = borrower_country_data.sort_values(by=['number_of_female_borrowers'], ascending=False)

# display the results

fig, ax = plt.subplots()

ax.bar(borrower_country_data.iloc[0:10,0], borrower_country_data.iloc[0:10,2],

label='Men', color='#7e81c4')

ax.bar(borrower_country_data.iloc[0:10,0], borrower_country_data.iloc[0:10,1],

bottom=borrower_country_data.iloc[0:10,2], label='Women', color='#cbcce7')

ax.set_xticklabels(labels=borrower_country_data.iloc[0:10,0], rotation = (90),

fontsize = 10, va='top', ha='left')

ax.set_ylabel('Number of borrowers')

ax.set_xlabel('Top 10 countries for women')

ax.set_title('NUMBER OF BORROWERS BY GENDER AND COUNTRY')

ax.legend()

plt.show()

The country with the highest number of female borrowers was the Philippines, it can also be observed that nearly all borrowers were women in Paraguay and Senegal, while India appears to consist of only female borrowers.

# create a pivot-table

tab7 = pd.pivot_table(loan_data_copy, values=['term_in_months', 'number_of_all_borrowers', 'number_of_male_borrowers', 'number_of_female_borrowers', 'loan_amount', 'funded_amount'], index=['repayment_interval'], aggfunc='sum')

# sort the results in descending order

tab7 = tab7.sort_values(by=['number_of_all_borrowers'], ascending=False)

# make some index entries into columns

tab7 = tab7.reset_index(level=['repayment_interval'])

# create another pivot-table

loan_repayment = pd.pivot_table(loan_data_copy, values='id', index=['repayment_interval'], aggfunc='count')

# sort the results in descending order

loan_repayment = loan_repayment.sort_values(by=['id'], ascending=False)

# rename the aggregated column to an appropiate label

loan_repayment.columns = ['number_of_loans']

# make some index entries into columns

loan_repayment = loan_repayment.reset_index(level=['repayment_interval'])

# initial status message

print('The shape of tab7 before merge: ', tab7.shape)

# join the data, keeping only relevant entries

tab7 = tab7.merge(loan_repayment, on='repayment_interval')

# final status message

print('The shape of tab7 after merge: ', tab7.shape)

The shape of tab7 before merge: (4, 7)

The shape of tab7 after merge: (4, 8)

# Present findings in more digestible formats by:

# 1. Converting total borrowers to male and female proportions

tab7.loc[:, 'female_pct_of_total_borrowers'] = round((tab7['number_of_female_borrowers']/tab7['number_of_all_borrowers'])*100, 2)

tab7.loc[:, 'male_pct_of_total_borrowers'] = round((tab7['number_of_male_borrowers']/tab7['number_of_all_borrowers'])*100, 2)

# 2. Extracting funding amounts based on gender

tab7.loc[:, 'million_USD_female_total_funding'] = round((tab7['female_pct_of_total_borrowers']/100*tab7['funded_amount'])/1000000, 2)

tab7.loc[:, 'million_USD_male_total_funding'] = round((tab7['male_pct_of_total_borrowers']/100*tab7['funded_amount'])/1000000, 2)

# 3. Extracting loan amounts based on gender

tab7.loc[:, 'million_USD_female_total_loan_amount'] = round((tab7['female_pct_of_total_borrowers']/100*tab7['loan_amount'])/1000000, 2)

tab7.loc[:, 'million_USD_male_total_loan_amount'] = round((tab7['male_pct_of_total_borrowers']/100*tab7['loan_amount'])/1000000, 2)

# 4. Extracting funding gaps based on gender

tab7.loc[:, 'million_female_funding_gap'] = -tab7['million_USD_female_total_loan_amount']+tab7['million_USD_female_total_funding']

tab7.loc[:, 'million_male_funding_gap'] = -tab7['million_USD_male_total_loan_amount']+tab7['million_USD_male_total_funding']

# drop raw data columns

tab7 = tab7.drop(['funded_amount', 'loan_amount',

'number_of_all_borrowers', 'number_of_female_borrowers',

'number_of_male_borrowers'],1)

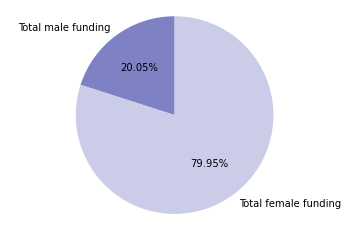

Funding received based on gender

# display summary of funding by gender

status = ['Total male funding','Total female funding']

values = [tab7['million_USD_male_total_funding'].sum(), tab7['million_USD_female_total_funding'].sum()]

fig1, ax1 = plt.subplots()

ax1.pie(values, labels=status,

autopct='%1.2f%%',

startangle=90,

colors=np.array(['#7e81c4','#cbcce7']))

ax1.axis('equal') # Equal aspect ratio ensures that pie is drawn as a circle.

plt.show()

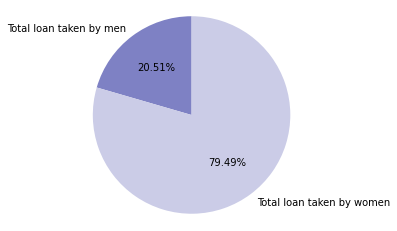

Total loan amounts taken by each gender

# display loan amounts by gender

status = ['Total loan taken by men','Total loan taken by women']

values = [tab7['million_USD_male_total_loan_amount'].sum(), tab7['million_USD_female_total_loan_amount'].sum()]

fig1, ax1 = plt.subplots()

ax1.pie(values, labels=status,

autopct='%1.2f%%',

startangle=90,

colors=np.array(['#7e81c4','#cbcce7']))

ax1.axis('equal') # Equal aspect ratio ensures that pie is drawn as a circle.

plt.show()

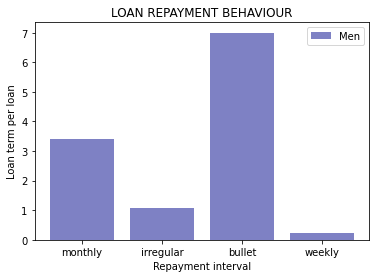

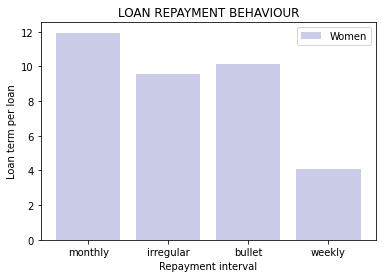

Loan repayment behaviour based on gender

# Display summary of loan repayment behaviour by gender

# 1. Men

fig, ax = plt.subplots()

ax.bar(tab7.iloc[:,0],

(tab7.iloc[:,1]/tab7.iloc[:,2])*(tab7.iloc[:,4]/100),

label='Men', color='#7e81c4')

ax.set_ylabel('Loan term per loan')

ax.set_xlabel('Repayment interval')

ax.set_title('LOAN REPAYMENT BEHAVIOUR')

ax.legend()

plt.show()

# 2. Women

fig, ax = plt.subplots()

ax.bar(tab7.iloc[:,0],

(tab7.iloc[:,1]/tab7.iloc[:,2])*(tab7.iloc[:,3]/100),

label='Women', color='#cbcce7')

ax.set_ylabel('Loan term per loan')

ax.set_xlabel('Repayment interval')

ax.set_title('LOAN REPAYMENT BEHAVIOUR')

ax.legend()

plt.show()

In as much as most men and women consistently paid off long-term loans on a monthly basis, women had a much larger time horizon to pay off their loans in general.

Additionally, a significant amount of data on repayment behaviour is missing for both genders (missing data is represented as the ‘bullet group’).

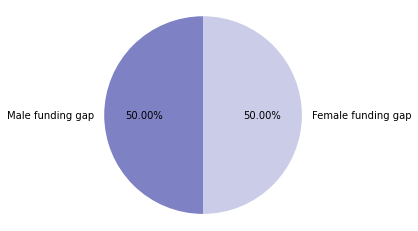

Funding gap in millions faced by each gender

# display summary of funding gap by gender

status = ['Male funding gap','Female funding gap']

values = [abs(tab7['million_male_funding_gap'].sum()), abs(tab7['million_male_funding_gap'].sum())]

fig1, ax1 = plt.subplots()

ax1.pie(values, labels=status,

autopct='%1.2f%%',

startangle=90,

colors=np.array(['#7e81c4','#cbcce7']))

ax1.axis('equal') # Equal aspect ratio ensures that pie is drawn as a circle.

plt.show()

print('In this instance, both men and women have the same size of funding gap, {} million US dollars\nover the time period the data was collected.'

.format(round(

abs(tab7['million_male_funding_gap'].sum()),

2)

)

)

In this instance, both men and women have the same size of funding gap, 10.19 million US dollars

over the time period the data was collected.

# display summary of the funding gap by gender and monthly repayment behaviour

fig, ax = plt.subplots()

ax.bar(tab7.iloc[:,0], tab7.iloc[:,10], label='Men', color='black')

ax.bar(tab7.iloc[:,0], tab7.iloc[:,9], bottom=tab7.iloc[:,10], label='Women', color='crimson')

ax.set_ylabel('Funding gap (millions)')

ax.set_xlabel('Repayment interval')

ax.set_title('SIZE OF FUNDING GAP')

ax.legend()

plt.show()

The graph above indicates that in as much as women are getting much more funding than men, those in the monthly repayment group still have a significant funding gap. Furthermore, the second-largest funding gap was not from those people belonging to the irregular payments group, but those belonging to the group that had missing data on payment behaviour. This makes sense because there may be a lack of trust that makes KIVA donors not foot the entire loan of those with missing repayment plans.

Global welfare#

In this section, we seek to explore the data to understand the financial well-being of various countries with the aid of an external dataset

1. What percentage of their monthly expenditure does the average citizen devote to loan repayments?

The purchasing power of various countries of the world can be visualized in the form of the monthly income table below:

# Made a copy of the data:

expenditure = PCE_data.copy()

# Convert any 'n/a' strings to NaN values

expenditure = expenditure.replace('n/a', np.nan)

# Convert any numeric data stored as a string into a decimal

cols = expenditure.columns[1:61]

for col in cols:

expenditure.loc[:,col] = expenditure[col].str.replace(',','')

for col in cols:

expenditure.loc[:,col] = expenditure[col].astype('float64')

MonthlyExpenditure = (expenditure.loc[:,'2013':'2017'].copy())/12

MonthlyExpenditure.loc[:,'country'] = expenditure['Country']

# Drop any null columns

MonthlyExpenditure = MonthlyExpenditure.dropna()

MonthlyExpenditure

| 2013 | 2014 | 2015 | 2016 | 2017 | country | |

|---|---|---|---|---|---|---|

| 1 | 582.357500 | 586.271667 | 584.475000 | 591.529167 | 592.816667 | American Samoa |

| 2 | 61.932500 | 63.661667 | 66.361667 | 69.737500 | 71.814167 | Cambodia |

| 3 | 175.452500 | 190.616667 | 206.155833 | 223.367500 | 243.301667 | China |

| 5 | 164.263333 | 170.690000 | 176.700000 | 183.363333 | 190.249167 | Indonesia |

| 6 | 121.336667 | 124.944167 | 137.075833 | 141.720833 | 145.214167 | Kiribati |

| ... | ... | ... | ... | ... | ... | ... |

| 179 | 91.753333 | 91.670000 | 92.621667 | 93.139167 | 93.662500 | Sudan |

| 180 | 42.089167 | 42.224167 | 43.976667 | 43.604167 | 43.282500 | Tanzania |

| 181 | 36.333333 | 37.132500 | 37.786667 | 38.175000 | 37.630833 | Togo |

| 182 | 54.592500 | 54.118333 | 57.973333 | 56.637500 | 54.675000 | Uganda |

| 184 | 84.350833 | 80.766667 | 94.590000 | 83.371667 | 83.315833 | Zimbabwe |

156 rows × 6 columns

In turn, the monthly repayments of various countries of the world can be visualized in the form of the monthly repayments table below:

# get the monthly repayment on each loan

loan_data_copy.loc[:, 'monthly_loan_repayment'] = loan_data_copy['loan_amount']/loan_data_copy['term_in_months']

# get the year that the loan was issued

loan_data_copy.loc[:,'disbursement_year'] = loan_data['disbursed_time'].dt.year

# create a pivot-table

tab8 = pd.pivot_table(loan_data_copy, values=['monthly_loan_repayment'], columns='disbursement_year', index=['country'], aggfunc='mean')

# drop level and rename columns

tab8 = tab8.droplevel('disbursement_year', axis=1)

tab8.columns = ['monthly_loan_repayment 2013', 'monthly_loan_repayment 2014',

'monthly_loan_repayment 2015', 'monthly_loan_repayment 2016',

'monthly_loan_repayment 2017']

# make some index entries into columns

tab8 = tab8.reset_index(level=['country'])

# and display all results

tab8

| country | monthly_loan_repayment 2013 | monthly_loan_repayment 2014 | monthly_loan_repayment 2015 | monthly_loan_repayment 2016 | monthly_loan_repayment 2017 | |

|---|---|---|---|---|---|---|

| 0 | Afghanistan | NaN | NaN | 750.000000 | 1333.333333 | NaN |

| 1 | Albania | 62.227835 | 64.557728 | 54.131447 | 55.527071 | 61.604227 |

| 2 | Armenia | 64.103653 | 64.558263 | 51.850628 | 49.406712 | 50.580462 |

| 3 | Azerbaijan | 105.071779 | 108.725509 | 82.548595 | 59.692751 | NaN |

| 4 | Belize | NaN | 18.405275 | NaN | 22.880435 | NaN |

| ... | ... | ... | ... | ... | ... | ... |

| 80 | Vanuatu | NaN | 62.500000 | NaN | NaN | NaN |

| 81 | Vietnam | 68.839701 | 91.272779 | 97.516549 | 90.730029 | 69.997056 |

| 82 | Yemen | 62.567830 | 57.303204 | 60.290609 | 43.056244 | 42.720586 |

| 83 | Zambia | NaN | 81.800068 | 93.311061 | 107.013918 | 74.278048 |

| 84 | Zimbabwe | 175.857143 | 74.398992 | 126.842706 | 110.083632 | 125.510372 |

85 rows × 6 columns

We need to find the countries shared in common between the Kiva.org and the UN dataset as follows:

# compare country/territory labels in the 2 datasets

print(tab8['country'].unique())

print('')

print(MonthlyExpenditure['country'].unique())

['Afghanistan' 'Albania' 'Armenia' 'Azerbaijan' 'Belize' 'Benin' 'Bhutan'

'Bolivia' 'Brazil' 'Burkina Faso' 'Burundi' 'Cambodia' 'Cameroon' 'Chile'

'China' 'Colombia' 'Congo' 'Costa Rica' "Cote D'Ivoire"

'Dominican Republic' 'Ecuador' 'Egypt' 'El Salvador' 'Georgia' 'Ghana'

'Guatemala' 'Haiti' 'Honduras' 'India' 'Indonesia' 'Iraq' 'Israel'

'Jordan' 'Kenya' 'Kosovo' 'Kyrgyzstan' "Lao People's Democratic Republic"

'Lebanon' 'Lesotho' 'Liberia' 'Madagascar' 'Malawi' 'Mali' 'Mauritania'

'Mexico' 'Moldova' 'Mongolia' 'Mozambique' 'Myanmar (Burma)' 'Namibia'

'Nepal' 'Nicaragua' 'Nigeria' 'Pakistan' 'Palestine' 'Panama' 'Paraguay'

'Peru' 'Philippines' 'Puerto Rico' 'Rwanda'

'Saint Vincent and the Grenadines' 'Samoa' 'Senegal' 'Sierra Leone'

'Solomon Islands' 'Somalia' 'South Africa' 'South Sudan' 'Suriname'

'Tajikistan' 'Tanzania' 'Thailand' 'The Democratic Republic of the Congo'

'Timor-Leste' 'Togo' 'Turkey' 'Uganda' 'Ukraine' 'United States'

'Vanuatu' 'Vietnam' 'Yemen' 'Zambia' 'Zimbabwe']

['American Samoa' 'Cambodia' 'China' 'Indonesia' 'Kiribati' 'Malaysia'

'Marshall Islands' 'Mongolia' 'Northern Mariana Islands' 'Palau'

'Philippines' 'Thailand' 'Timor-Leste' 'Vietnam' 'Albania' 'Armenia'

'Belarus' 'Bosnia and Herzegovina' 'Bulgaria' 'Croatia' 'Czech Republic'

'Estonia' 'Georgia' 'Hungary' 'Kazakhstan' 'Kosovo' 'Kyrgyz Republic'

'Latvia' 'Lithuania' 'Moldova' 'Montenegro' 'North Macedonia' 'Poland'

'Romania' 'Russian Federation' 'Serbia' 'Slovak Republic' 'Slovenia'

'Turkey' 'Ukraine' 'Uzbekistan' 'Argentina' 'Belize' 'Bolivia' 'Brazil'

'Chile' 'Colombia' 'Costa Rica' 'Cuba' 'Dominican Republic' 'Ecuador'

'El Salvador' 'Guatemala' 'Haiti' 'Honduras' 'Jamaica' 'Mexico'

'Nicaragua' 'Panama' 'Paraguay' 'Peru' 'Uruguay' 'Algeria'

'Egypt, Arab Republic of' 'Iran, Islamic Republic of' 'Jordan' 'Lebanon'

'Morocco' 'Oman' 'West Bank and Gaza' 'Australia' 'Austria'

'Bahamas, The' 'Bahrain' 'Belgium' 'Brunei Darussalam' 'Canada' 'Cyprus'

'Denmark' 'Finland' 'France' 'Germany' 'Greece' 'Greenland' 'Guam'

'Hong Kong SAR, China' 'Iceland' 'Ireland' 'Israel' 'Italy' 'Japan'

'Korea, Republic of' 'Kuwait' 'Luxembourg' 'Macao SAR, China'

'Netherlands' 'New Zealand' 'Norway' 'Portugal' 'Puerto Rico'

'Saudi Arabia' 'Singapore' 'Spain' 'Sweden' 'Switzerland'

'United Arab Emirates' 'United Kingdom' 'United States'

'Virgin Islands, US' 'Bangladesh' 'Bhutan' 'India' 'Nepal' 'Pakistan'

'Sri Lanka' 'Angola' 'Benin' 'Botswana' 'Burkina Faso' 'Burundi'

'Cabo Verde' 'Cameroon' 'Central African Republic' 'Chad' 'Comoros'

'Congo, Democratic Republic of' 'Congo, Republic of' "Cote d'Ivoire"

'Equatorial Guinea' 'Eswatini' 'Gabon' 'Gambia, The' 'Ghana' 'Guinea'

'Guinea-Bissau' 'Kenya' 'Lesotho' 'Liberia' 'Madagascar' 'Malawi' 'Mali'

'Mauritania' 'Mauritius' 'Mozambique' 'Namibia' 'Niger' 'Nigeria'

'Rwanda' 'Senegal' 'Sierra Leone' 'South Africa' 'Sudan' 'Tanzania'

'Togo' 'Uganda' 'Zimbabwe']

# MATCH COUNTRIES IN KIVA LOAN DATA AND THOSE IN THE ORIGINAL DATASET IF THEY HAVE DIFFERENT SPELLINGS

tab8.iloc[16,0] = 'Congo, Republic of'

tab8.iloc[18,0] = "Cote d'Ivoire"

tab8.iloc[21,0] = 'Egypt, Arab Republic of'

tab8.iloc[35,0] = 'Kyrgyz Republic'

tab8.iloc[48,0] = 'Myanmar'

tab8.iloc[54,0] = 'West Bank and Gaza'

# tab8.iloc[61,0] missing in other dataset

# tab8.iloc[62,0] missing in other dataset; only have American Samoa

# tab8.iloc[63,0] missing in other dataset

# tab8.iloc[65,0] missing in other dataset

# tab8.iloc[66,0] missing in other dataset

tab8.iloc[73,0] = 'Congo, Democratic Republic of'

# tab8.iloc[82,0] missing in other dataset

#CHECK FOR COUNTRIES NOT WITHIN EITHER ONE OF THE DATASET

tab8[tab8['country'].isin(MonthlyExpenditure['country']) == False]

| country | monthly_loan_repayment 2013 | monthly_loan_repayment 2014 | monthly_loan_repayment 2015 | monthly_loan_repayment 2016 | monthly_loan_repayment 2017 | |

|---|---|---|---|---|---|---|

| 0 | Afghanistan | NaN | NaN | 750.000000 | 1333.333333 | NaN |

| 3 | Azerbaijan | 105.071779 | 108.725509 | 82.548595 | 59.692751 | NaN |

| 30 | Iraq | 173.604827 | 198.899334 | 186.551621 | NaN | NaN |

| 36 | Lao People's Democratic Republic | NaN | 122.887368 | 76.689249 | 78.100108 | 55.966610 |

| 48 | Myanmar | NaN | 1084.647495 | 301.828805 | 153.652721 | 80.601104 |

| 61 | Saint Vincent and the Grenadines | NaN | 43.601190 | 91.355946 | NaN | NaN |

| 62 | Samoa | 45.125878 | 64.451621 | 56.148887 | 63.796669 | 60.880531 |

| 65 | Solomon Islands | NaN | 50.795455 | 64.064459 | 79.784429 | 69.712160 |

| 66 | Somalia | NaN | 272.774699 | 230.544232 | 564.285714 | 510.714286 |

| 68 | South Sudan | NaN | 75.533234 | 44.681710 | NaN | 6250.000000 |

| 69 | Suriname | NaN | 331.387203 | 232.768221 | 263.640545 | NaN |

| 70 | Tajikistan | 67.230372 | 66.099868 | 53.060960 | 40.184397 | 37.572885 |

| 80 | Vanuatu | NaN | 62.500000 | NaN | NaN | NaN |

| 82 | Yemen | 62.567830 | 57.303204 | 60.290609 | 43.056244 | 42.720586 |

| 83 | Zambia | NaN | 81.800068 | 93.311061 | 107.013918 | 74.278048 |

The table above shows countries that are missing in either of the datasets and will not be included.

The percentage of monthly expenditure that the average citizen devote to loan repayments is visualized below:

# initial status message

print('The shape of tab8 before merge: ', tab8.shape)

# join the data, keeping only relevant entries

tab8 = tab8.merge(MonthlyExpenditure, on='country')

# final status message

print('The shape of tab8 after merge: ', tab8.shape)

The shape of tab8 before merge: (85, 6)

The shape of tab8 after merge: (70, 11)

years = ['2013','2014','2015','2016','2017']

for year in years:

tab8.loc[:, f'% of monthly expenditure, {year}'] = (tab8[f'monthly_loan_repayment {year}']/tab8[f'{year}']) * 100

tab8[f'% of monthly expenditure, {year}'] = round(tab8[f'% of monthly expenditure, {year}'], 2)

tab8 = tab8.drop([f'monthly_loan_repayment {year}',f'{year}'], axis=1)

# sort the results in descending order

tab8 = tab8.sort_values(by=['% of monthly expenditure, 2017'], ascending=False)

fig, ax = plt.subplots()

ax.bar(tab8.head(10).iloc[:,0],

tab8.head(10)['% of monthly expenditure, 2017'],

color='crimson')

#plt.ylabel('Funding gap per loan')

ax.set_xticklabels(labels=tab8.head(10).iloc[:,0], rotation = (90), fontsize = 10, va='top', ha='left')

#plt.xlabel('Sectors')

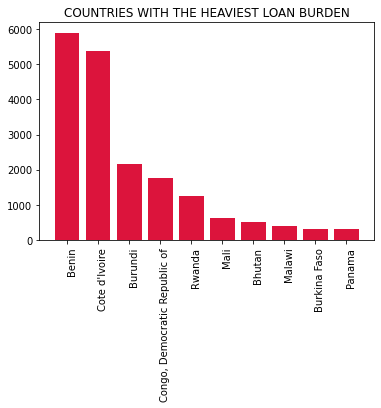

plt.title('COUNTRIES WITH THE HEAVIEST LOAN BURDEN')

plt.show()

print ('\n')

fig, ax = plt.subplots()

ax.bar(tab8.tail(10).iloc[:,0],

tab8.tail(10)['% of monthly expenditure, 2017'],

color='green')

#plt.ylabel('Funding gap per loan')

ax.set_xticklabels(labels=tab8.tail(10).iloc[:,0], rotation = (90), fontsize = 10, va='top', ha='left')

#plt.xlabel('Sectors')

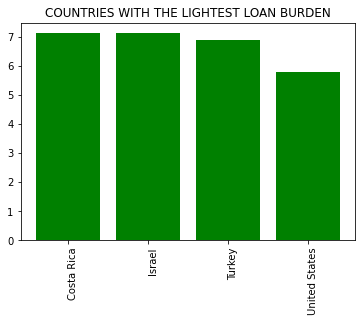

plt.title('COUNTRIES WITH THE LIGHTEST LOAN BURDEN')

plt.show()

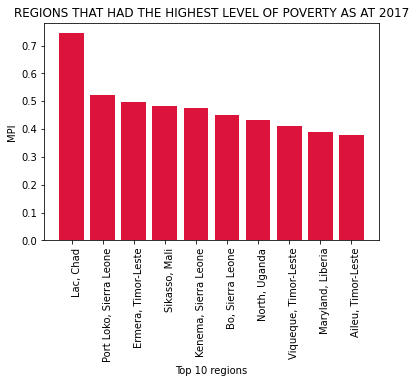

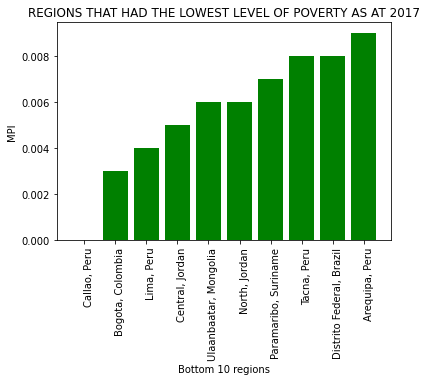

2. What geographical regions have the highest and lowest levels of poverty?

This is measured by the Multidimensional Poverty Index (MPI). This was obtained as follows:

print(loan_data_copy.shape)

print('Number of null values in the "region" column: ',loan_data_copy['region'].isnull().sum())

print('Number of null values in the "country_code" column: ',loan_data_copy['country_code'].isnull().sum())

print('Number of null values in the "country" column: ',loan_data_copy['country'].isnull().sum())

print('')

print('N/B: ', loan_data_copy[loan_data_copy['region'].isin(location_data['region']) == False].shape[0],

'number of loan records have regions that are not covered in both datasets.')

print(' ', loan_data_copy[loan_data_copy['country'].isin(location_data['country']) == False].shape[0],

'number of loan records have countries that are not covered in both datasets.')

(671205, 26)

Number of null values in the "region" column: 56800

Number of null values in the "country_code" column: 8

Number of null values in the "country" column: 0

N/B: 558379 number of loan records have regions that are not covered in both datasets.

80765 number of loan records have countries that are not covered in both datasets.

Based on country:

# Let's first get a national average for MPI

# create a pivot-table

tab9 = pd.pivot_table(location_data, values=['MPI'], index=['country'], aggfunc='min')

# rename the MPI

tab9.columns = ['national_minimum_of_MPI']

# make some index entries into columns

tab9 = tab9.reset_index(level=['country'])

# sort the results in descending order

tab9 = tab9.sort_values(by=['national_minimum_of_MPI'], ascending=False)

# display all results

fig, ax = plt.subplots()

ax.bar(tab9.iloc[0:10,0], tab9.iloc[0:10,1], color='crimson')

plt.ylabel('MPI (national minimum)')

ax.set_xticklabels(labels=tab9.iloc[0:10,0], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Top 10 countries')

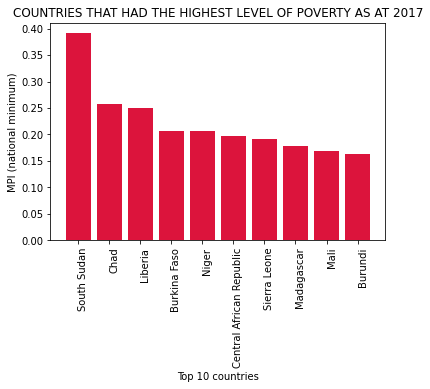

plt.title('COUNTRIES THAT HAD THE HIGHEST LEVEL OF POVERTY AS AT 2017')

plt.show()

print('\n')

# sort the results in ascending order

tab9 = tab9.sort_values(by=['national_minimum_of_MPI'], ascending=True)

# display all results

fig, ax = plt.subplots()

ax.bar(tab9.iloc[0:10,0], tab9.iloc[0:10,1], color='green')

plt.ylabel('MPI (national minimum)')

ax.set_xticklabels(labels=tab9.iloc[0:10,0], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Bottom 10 countries')

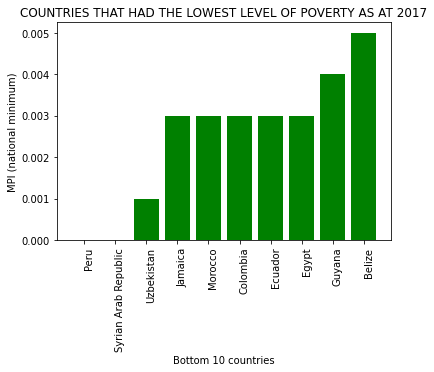

plt.title('COUNTRIES THAT HAD THE LOWEST LEVEL OF POVERTY AS AT 2017')

plt.show()

Based on the results above, countries with high MPI values are not receiving the most funding - in fact, El-Salvador, a country with one of the lowest MPI scores was one of the top 10 countries that received the most funding.

Based on in-country regions:

region_data = loan_data_copy[loan_data_copy['region'].isin(location_data['region']) == True]

region_data = region_data.copy()

tab10 = pd.pivot_table(region_data, values=['funded_amount', 'loan_amount',

'number_of_all_borrowers', 'monthly_loan_repayment'],

index=['region'], aggfunc='sum')

# make some index entries into columns

tab10 = tab10.reset_index(level=['region'])

tab11 = pd.pivot_table(region_data, values=['id'],

index=['region'], aggfunc='count')

# rename the aggregated column

tab11.columns = ['number_of_loans']

# make some index entries into columns

tab11 = tab11.reset_index(level=['region'])

# initial status message

print('The shape of tab10 before merge: ', tab10.shape)

# join the data, keeping only relevant entries

tab10 = tab10.merge(tab11, on='region')

# final status message

print('The shape of tab10 after merge: ', tab10.shape)

# initial status message

print('The shape of tab10 before merge: ', tab10.shape)

# join the data, keeping only relevant entries

tab10 = tab10.merge(location_data, on='region')

# final status message

print('The shape of tab10 after merge: ', tab10.shape)

The shape of tab10 before merge: (131, 5)

The shape of tab10 after merge: (131, 6)

The shape of tab10 before merge: (131, 6)

The shape of tab10 after merge: (144, 14)

# sort the results in descending order

tab10 = tab10.sort_values(by=['MPI'], ascending=False)

# display all results

fig, ax = plt.subplots()

ax.bar(tab10.iloc[0:10,6], tab10.iloc[0:10,10], color='crimson')

plt.ylabel('MPI')

ax.set_xticklabels(labels=tab10.iloc[0:10,6], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Top 10 regions')

plt.title('REGIONS THAT HAD THE HIGHEST LEVEL OF POVERTY AS AT 2017')

plt.show()

print('\n')

# sort the results in ascending order

tab10 = tab10.sort_values(by=['MPI'], ascending=True)

# display all results

fig, ax = plt.subplots()

ax.bar(tab10.iloc[0:10,6], tab10.iloc[0:10,10], color='green')

plt.ylabel('MPI')

ax.set_xticklabels(labels=tab10.iloc[0:10,6], rotation = (90), fontsize = 10, va='top', ha='left')

plt.xlabel('Bottom 10 regions')

plt.title('REGIONS THAT HAD THE LOWEST LEVEL OF POVERTY AS AT 2017')

plt.show()

Peru has the third highest number of loans and it is the third most funded country; based on the graph above, it has 3 regions among countries with the lowest MPI scores with the fourth region having an unknown MPI score.

Conclusions#

The welfare of borrowers that receive the largest amount of funding on Kiva can be viewed as good because:

Women form the bulk of the borrowers and they receive the highest number of funds, even as they have the highest shortfall.

Countries like Peru and El Salvador which based on the data have low MPI scores have received a lot of funding

The most valuable partnerships are those with social impact businesses, which implies that they are able to hanle regular payments as they make an income from their goods and services

Few borrowers are taking loans for personal use

Kenya and the Phillipines have a lot of funding for small loans; this implies that massive impact is being achieved in these countries because the loans are small enough to pay back and monthly repayments are taking up only 50% or less of their monthly income

With that said, it is concerning to see that countries that have many more people in need are not accessing large amounts of funds; furthermore, even when they do, places like Burkina Faso, Sierra Leone and Mali had a high debt burden, trapping borrowers from these countries in poverty.